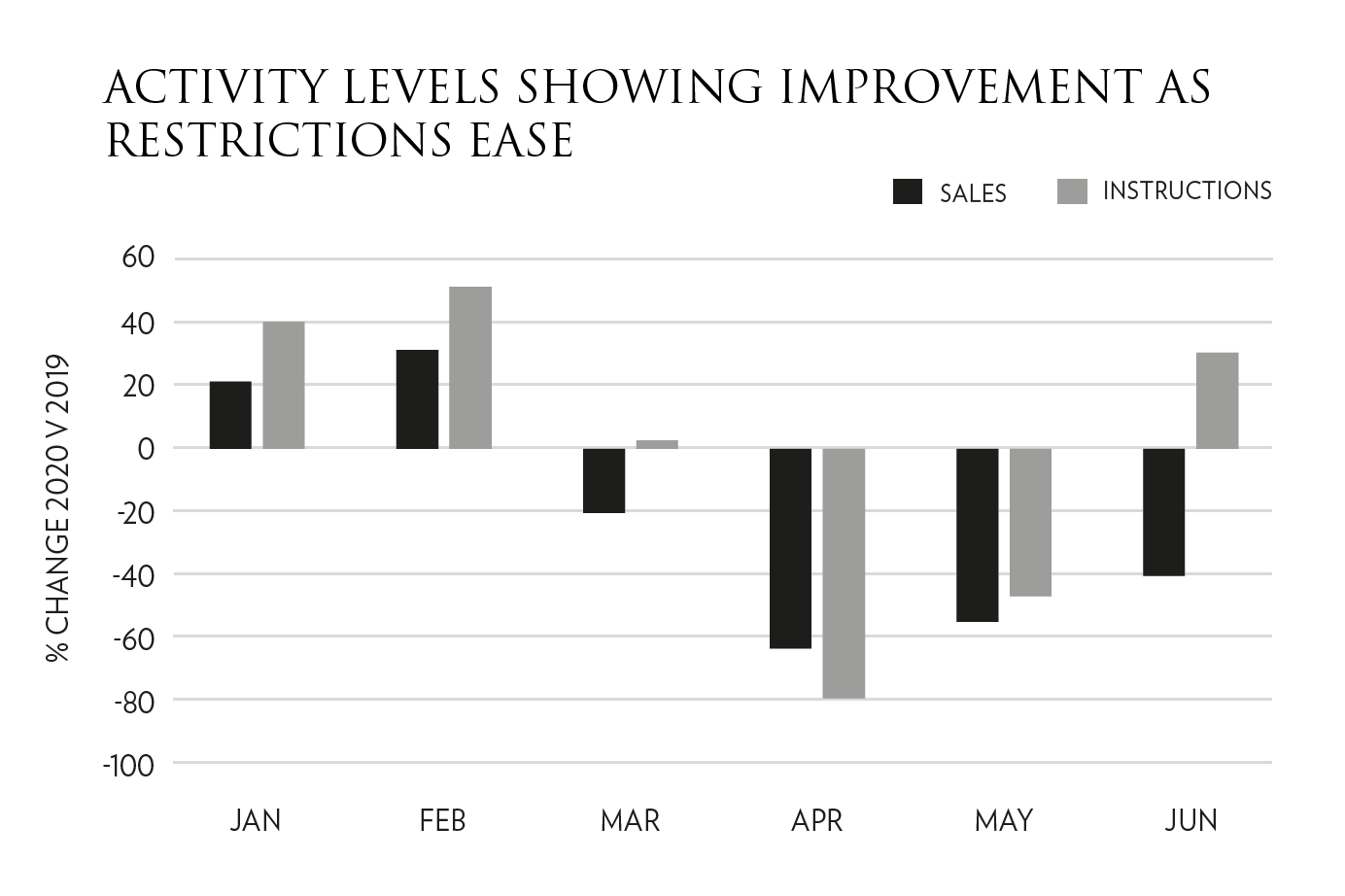

Following a positive start to 2020 with sales volumes and levels of new instructions up yearon-year COVID-19 created a seismic shock wave as activity across the housing market halted. When the market reopened on 13th May the positive sentiment from a release of pent-up demand was immediate and has been sustained. The majority (92%) of London buyers who had been searching pre lockdown still intend to purchase, two-thirds actively looking to buy as soon as they find the right home or sell their existing property. Across prime London, Savills reported a 32% increase in new buyer registrations in June compared to the average in the ten weeks pre-lockdown, with new instructions in June up 30% year-on-year according to LonRes.

Following a positive start to 2020 with sales volumes and levels of new instructions up yearon-year COVID-19 created a seismic shock wave as activity across the housing market halted. When the market reopened on 13th May the positive sentiment from a release of pent-up demand was immediate and has been sustained. The majority (92%) of London buyers who had been searching pre lockdown still intend to purchase, two-thirds actively looking to buy as soon as they find the right home or sell their existing property. Across prime London, Savills reported a 32% increase in new buyer registrations in June compared to the average in the ten weeks pre-lockdown, with new instructions in June up 30% year-on-year according to LonRes.

Knight Frank report the number of offers agreed across prime London below £1 million since May 13th is 41% higher than the five-year average, with offers agreed for properties priced £5 million plus rising by 10%. LonRes assert achieved prices in Q2 were just 0.5% lower than during Q1 2020, with vendors holding steady on prices. Price reductions of 8.9% are on par with Q1 (8.6%) and lower than during 2019. Savills predict prime London prices will be just 2% lower year-on-year in 2020 before returning to growth in 2021.

Knight Frank report the number of offers agreed across prime London below £1 million since May 13th is 41% higher than the five-year average, with offers agreed for properties priced £5 million plus rising by 10%. LonRes assert achieved prices in Q2 were just 0.5% lower than during Q1 2020, with vendors holding steady on prices. Price reductions of 8.9% are on par with Q1 (8.6%) and lower than during 2019. Savills predict prime London prices will be just 2% lower year-on-year in 2020 before returning to growth in 2021.

The current unknown is whether market activity will continue over the longer term, due to the wider economic impact of COVID-19. The announcement of the removal of stamp duty up to £500,000 will benefit house buyers and investors alike. Overseas purchasers will be buoyed by the easing of travel restrictions and the relative value of sterling still offers discounts against many currencies. London is still considered a safe haven for investment, and according to research by Savills, at 13.9% the cost of buying, holding and selling property in the UK2 is less expensive than other global cities including Vancouver, New York and Hong Kong. London remains appealing.

Past issues

- Spring 2014

- Summer 2014

- Autumn 2014

- Winter 2015

- Spring 2015

- Autumn 2015

- Winter 2016

- Spring 2016

- Summer 2016

- Autumn 2016

- Winter 2017

- Spring 2017

- Summer 2017

- Autumn 2017

- Winter 2018

- Spring 2018

- Summer 2018

- Autumn 2018

- Winter 2019

- Spring 2019

- Summer 2019

- Autumn 2019

- Winter 2020

- Summer 2020

- Autumn 2022

- Winter 2023

- Spring 2023